The Consumer's Problem: Review

- The consumer's constrained optimization problem is:

Choose: < a consumption bundle >

In order to maximize: < utility >

Subject to: < income and market prices >

The Consumer's Problem: Tools

We now have the tools to understand consumer choices:

Budget constraint: consumer's constraints of income and market prices

- How the .red[market] trades off between two goods

- Utility function: consumer's preferences to maximize

- How the .green[consumer] trades off between two goods

The Consumer's Problem: Verbally

- The consumer's constrained optimization problem:

choose a bundle of goods to maximize utility, subject to income and market prices

The Consumer's Problem: Mathematically

maxx,yu(x,y)

- This requires calculus to solve1. We will look at graphs instead!

1 See the mathematical appendix in today's class notes on how to solve it with calculus, and an example.

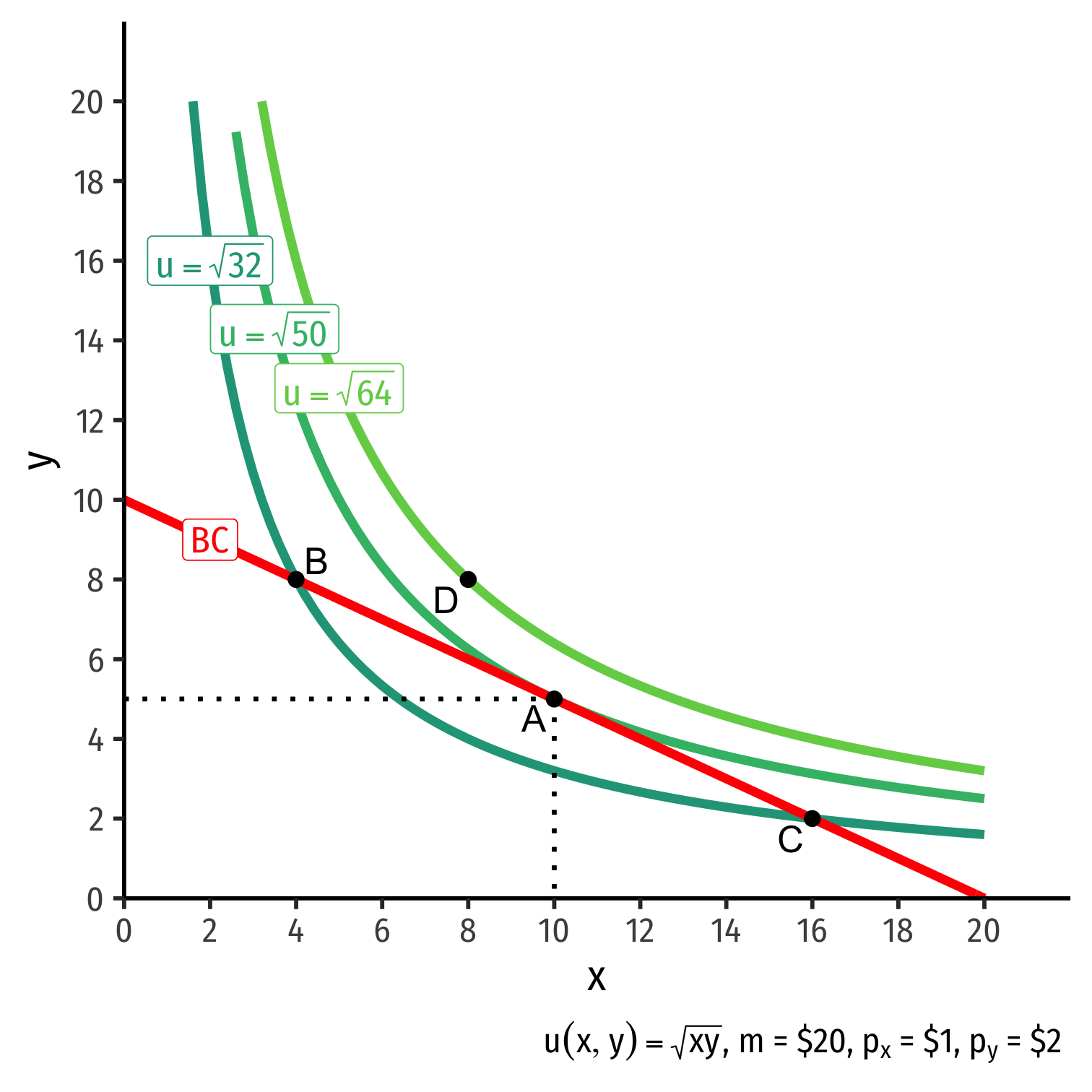

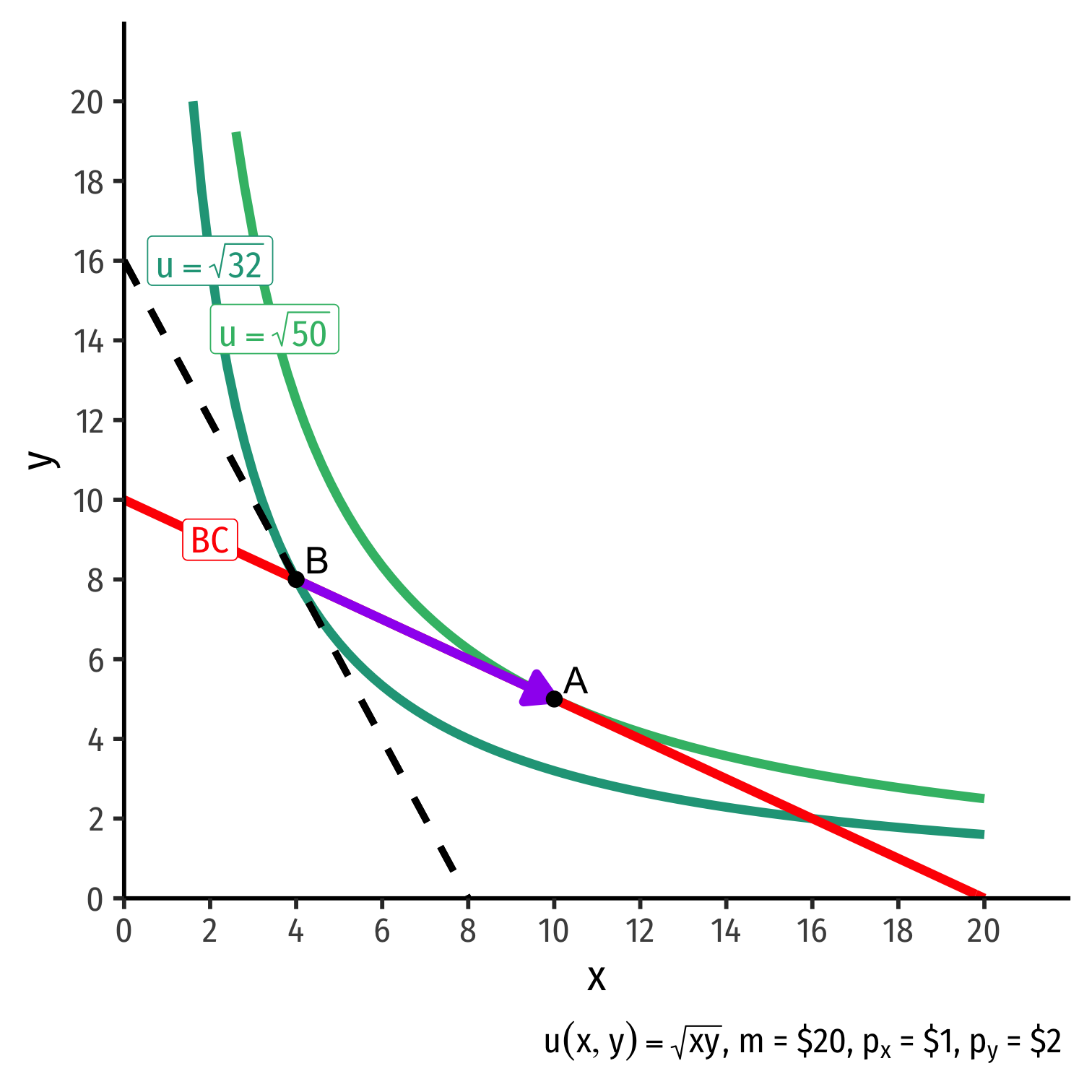

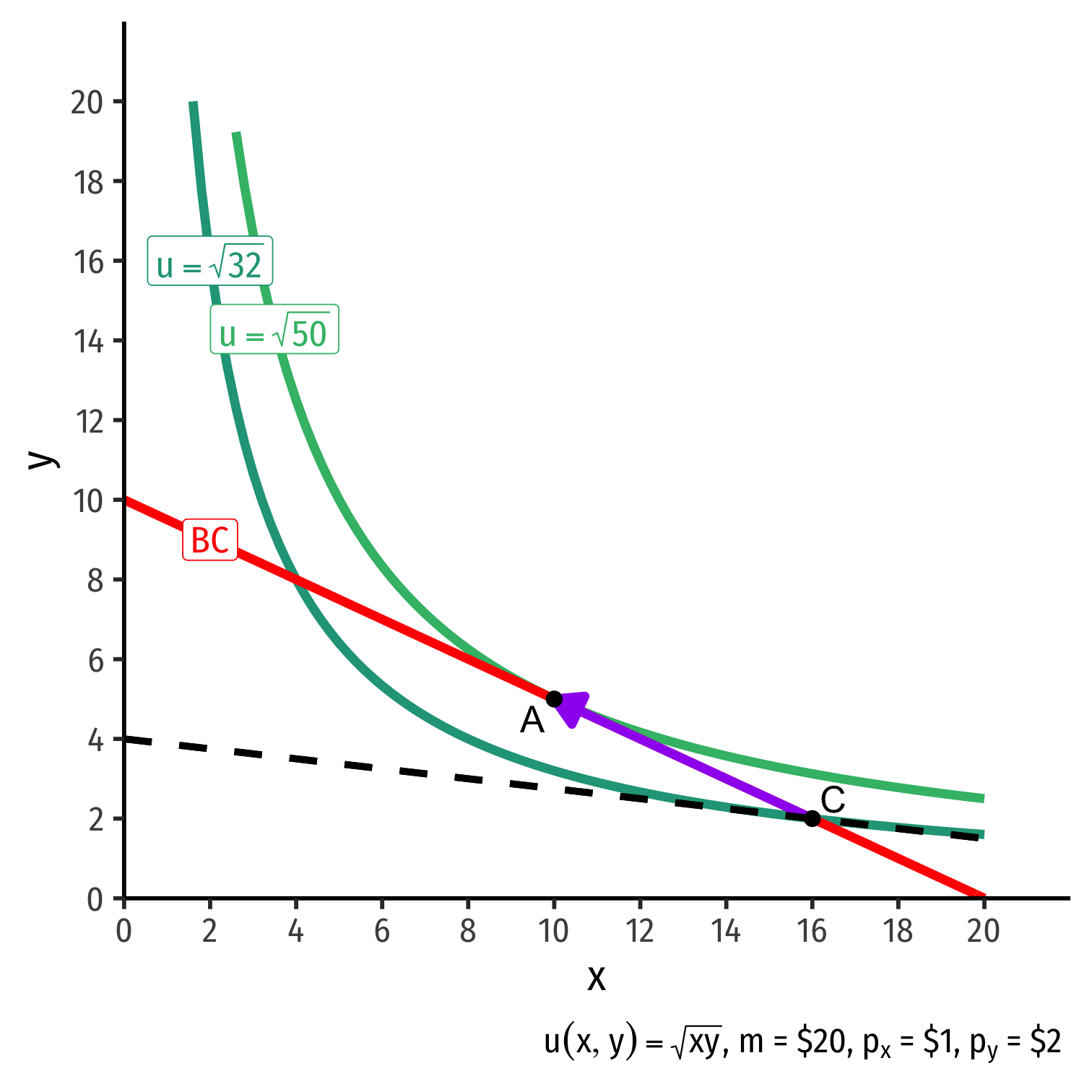

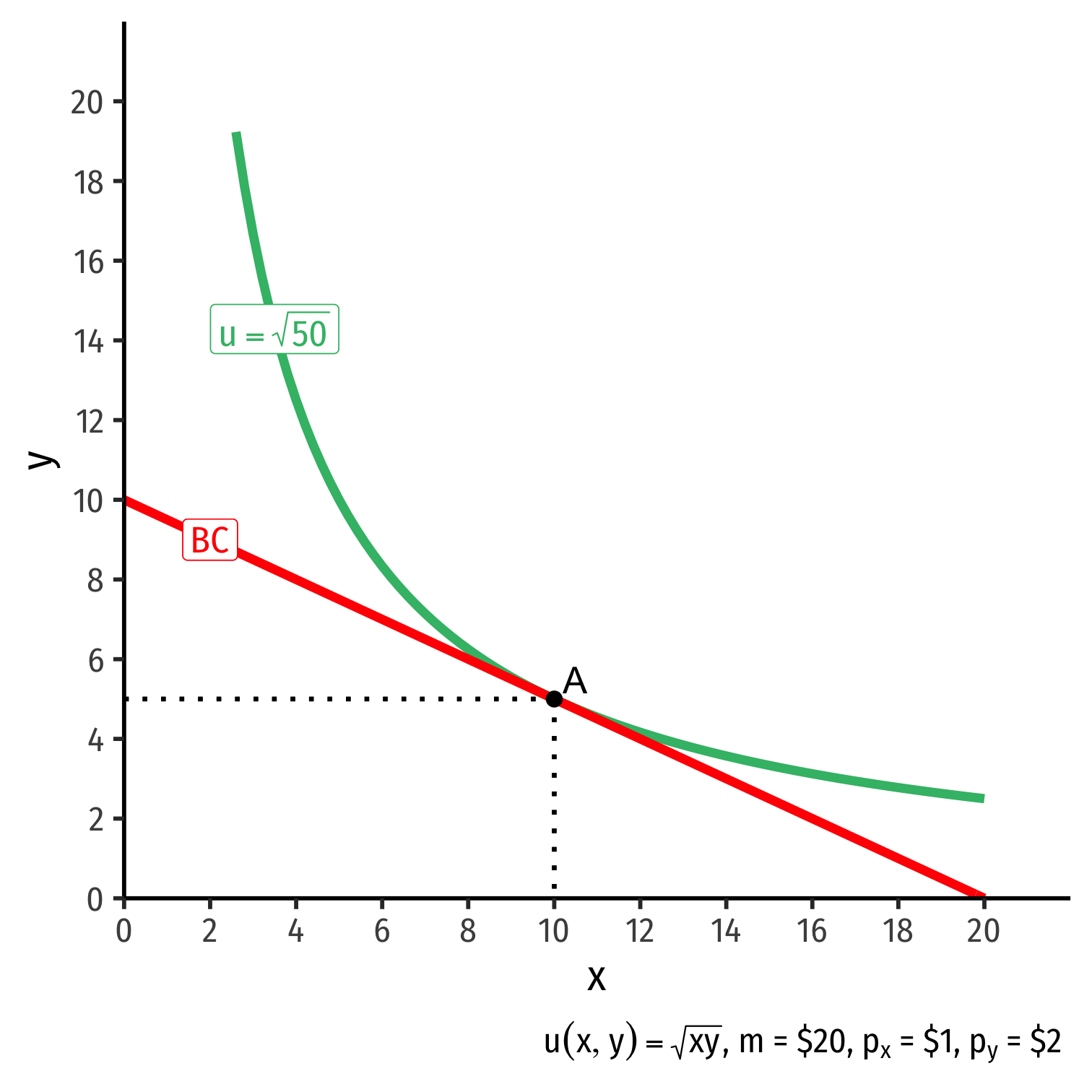

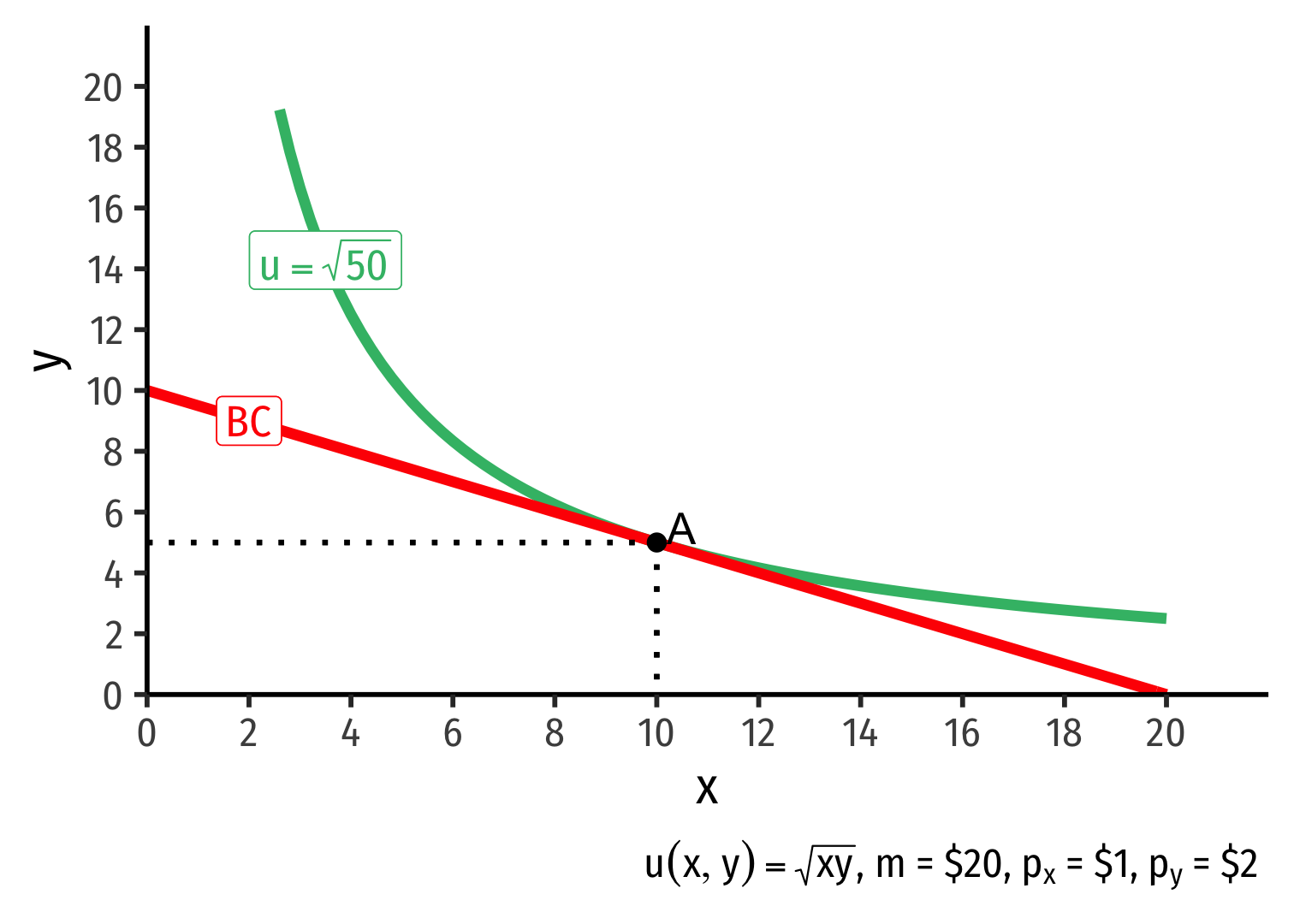

The Consumer's Optimum: Graphically

- Graphical solution: Highest indifference curve tangent to budget constraint

- Bundle A!

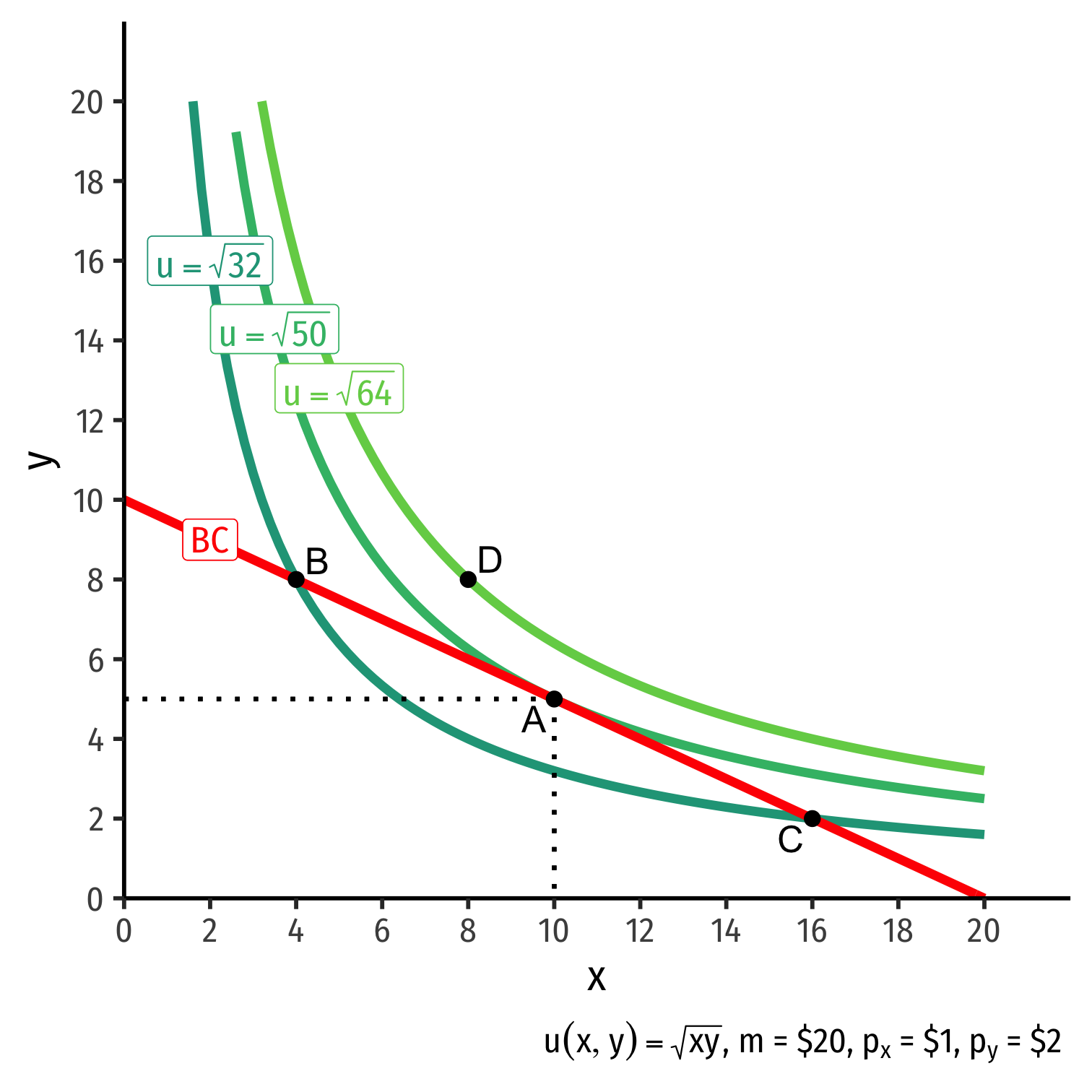

The Consumer's Optimum: Graphically

Graphical solution: Highest indifference curve tangent to budget constraint

- Bundle A!

B or C spend all income, but a better combination exists

- Averages ≻ extremes!

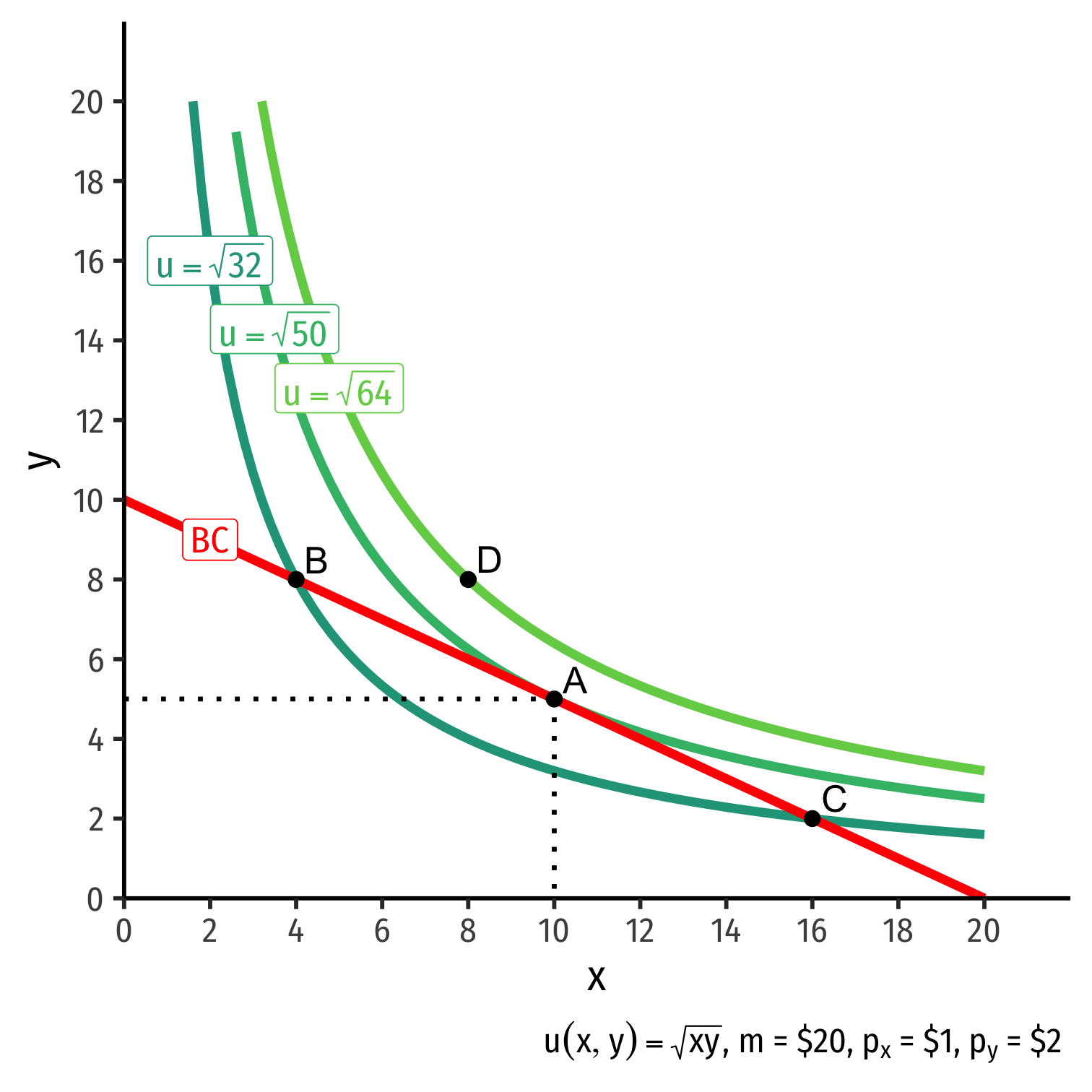

The Consumer's Optimum: Graphically

Graphical solution: Highest indifference curve tangent to budget constraint

- Bundle A!

B or C spend all income, but a better combination exists

- Averages ≻ extremes!

D is higher utility, but not affordable at current income & prices

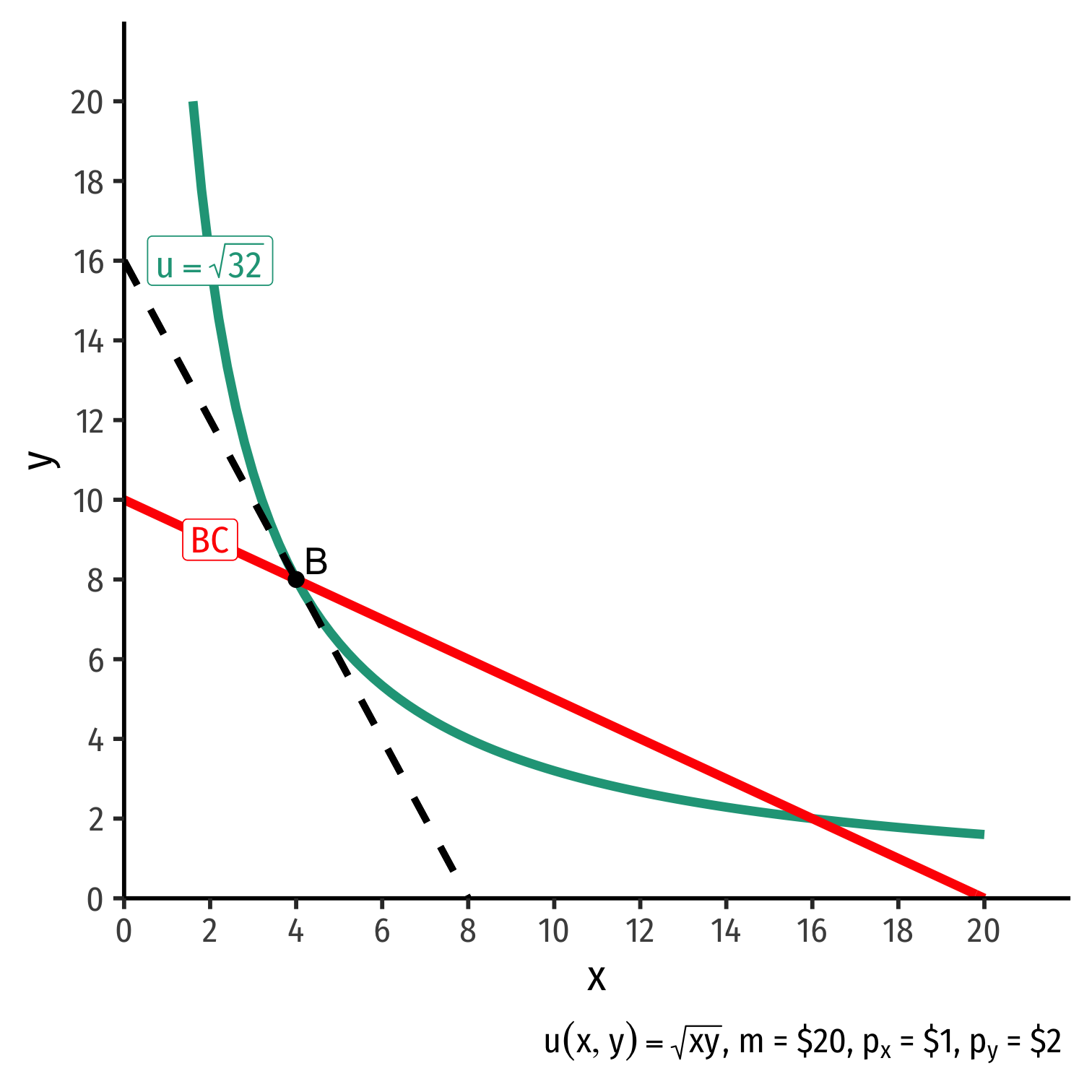

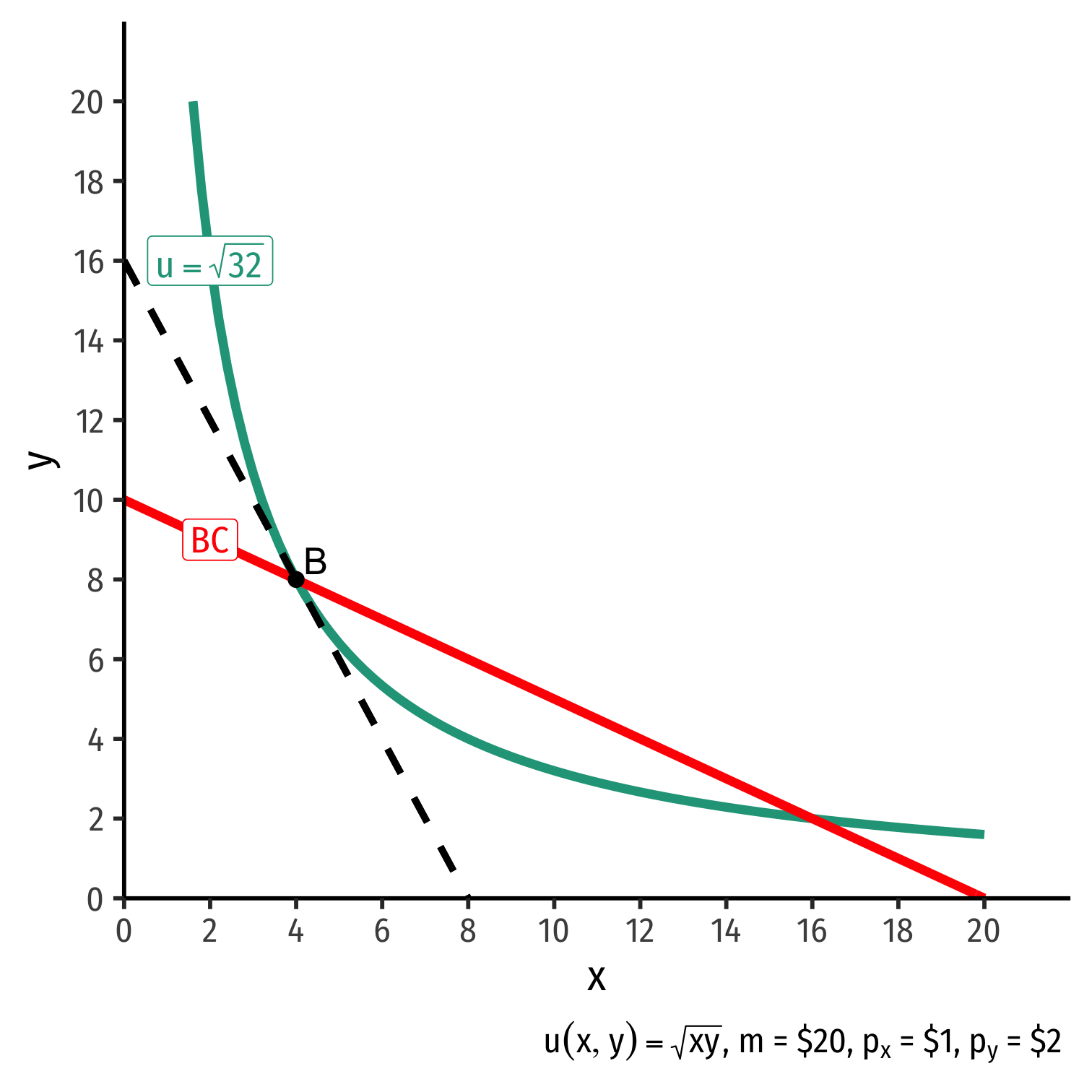

The Consumer's Optimum: Why Not B?

indiff. curve slope>budget constr. slope

The Consumer's Optimum: Why Not B?

indiff. curve slope>budget constr. slope|MRSx,y|>|pxpy||MUxMUy|>|pxpy||−2|>|−0.5|

Consumer would exchange at 2Y:1X

Market exchange rate is 0.5Y:1X

The Consumer's Optimum: Why Not B?

indiff. curve slope>budget constr. slope|MRSx,y|>|pxpy||MUxMUy|>|pxpy||−2|>|−0.5|

Consumer would exchange at 2Y:1X

Market exchange rate is 0.5Y:1X

Can spend less on y more on x and get more utility!

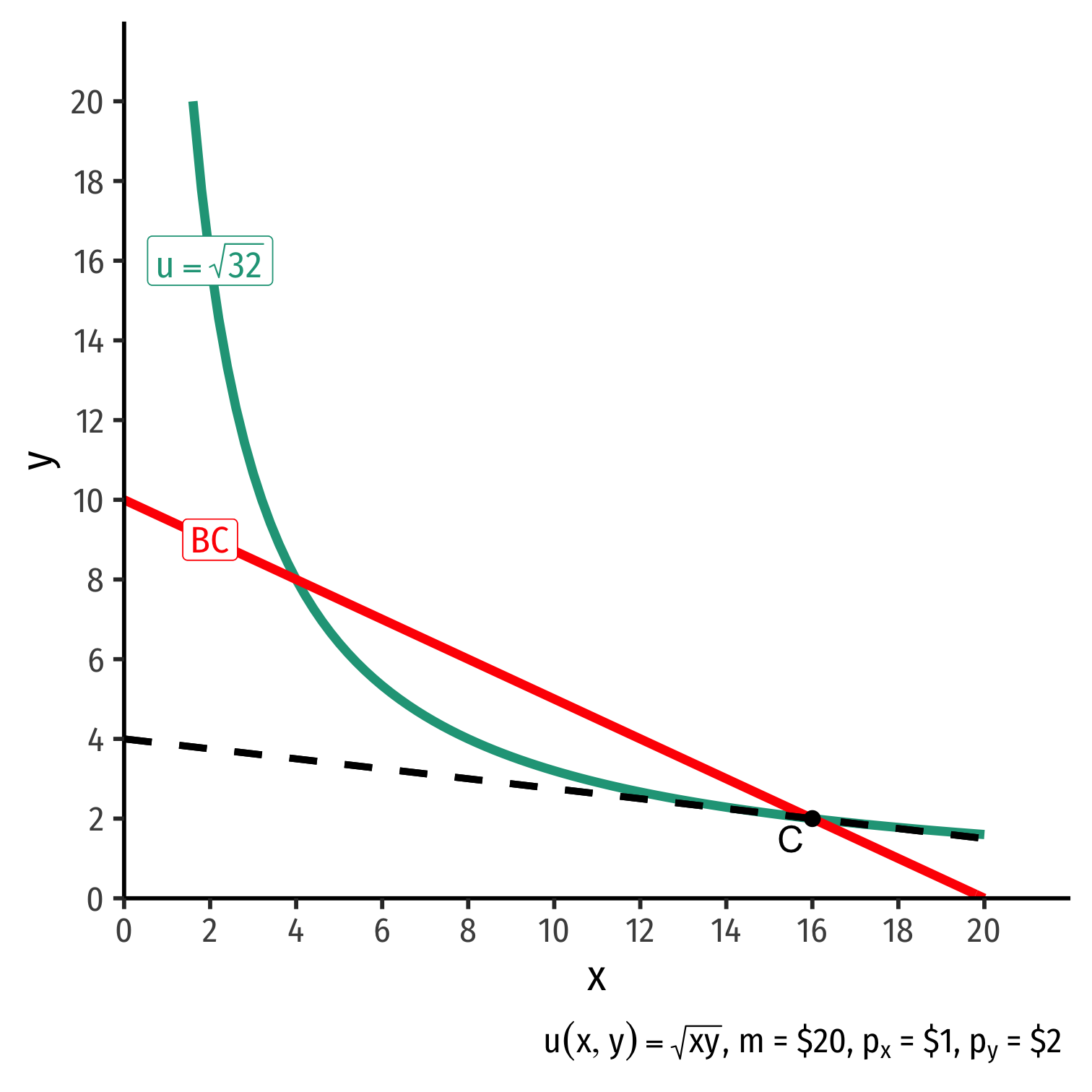

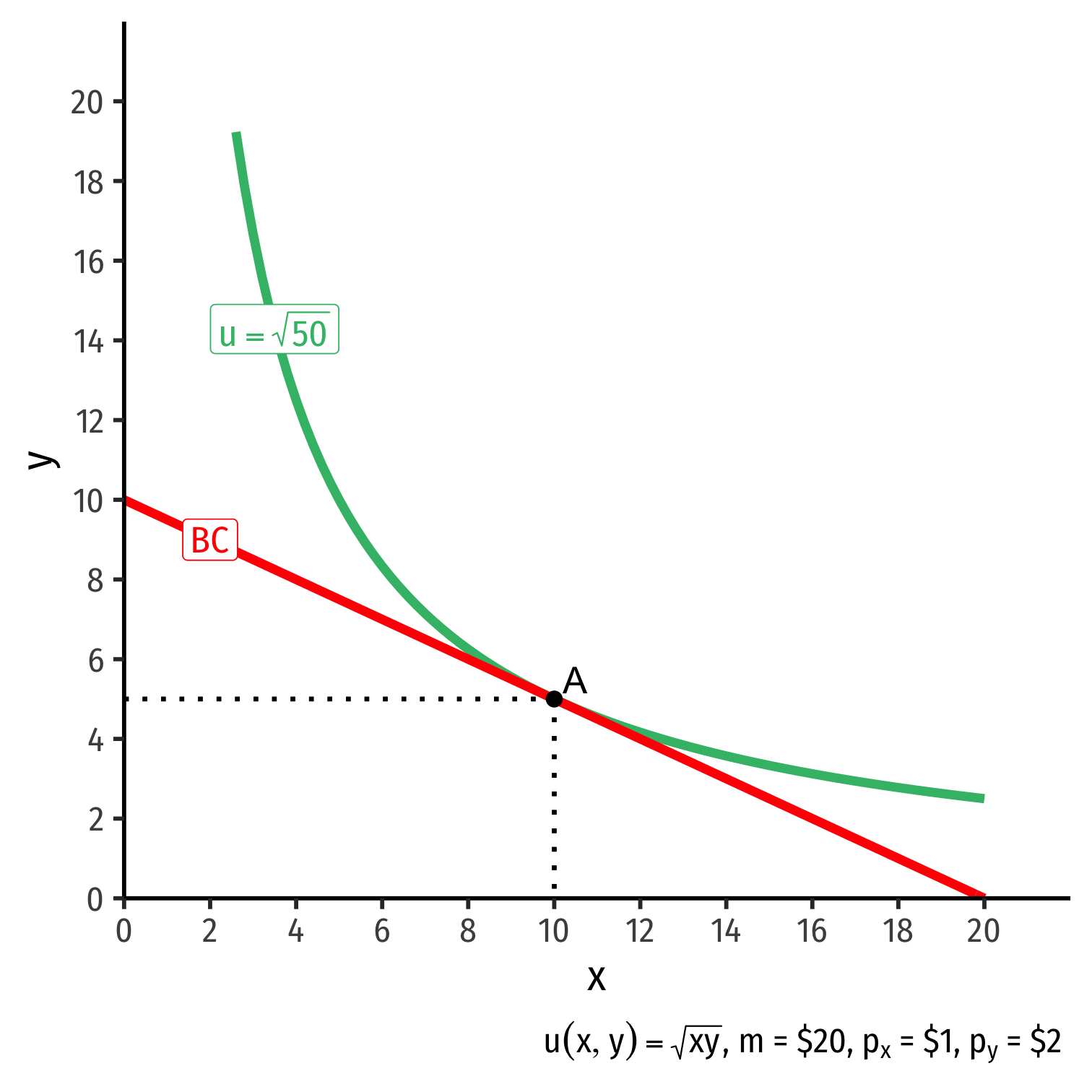

The Consumer's Optimum: Why Not C?

indiff. curve slope<budget constr. slope

The Consumer's Optimum: Why Not C?

indiff. curve slope<budget constr. slope|MRSx,y|<|pxpy||MUxMUy|<|pxpy||−0.125|<|−0.5|

Consumer would exchange at 0.125Y:1X

Market exchange rate is 0.5Y:1X

The Consumer's Optimum: Why Not C?

indiff. curve slope<budget constr. slope|MRSx,y|<|pxpy||MUxMUy|<|pxpy||−0.125|<|−0.5|

Consumer would exchange at 0.125Y:1X

Market exchange rate is 0.5Y:1X

Can spend less on x, more on y and get more utility!

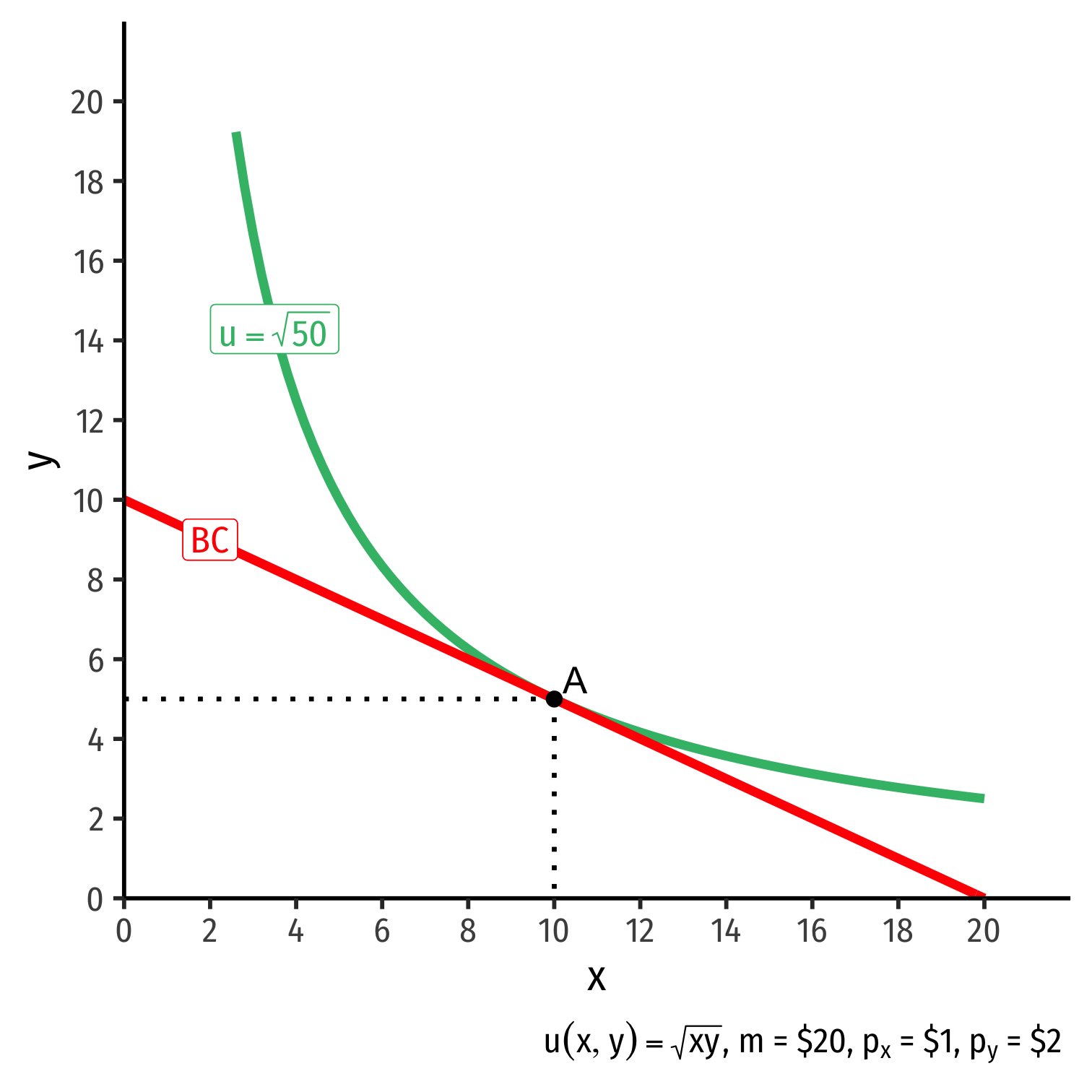

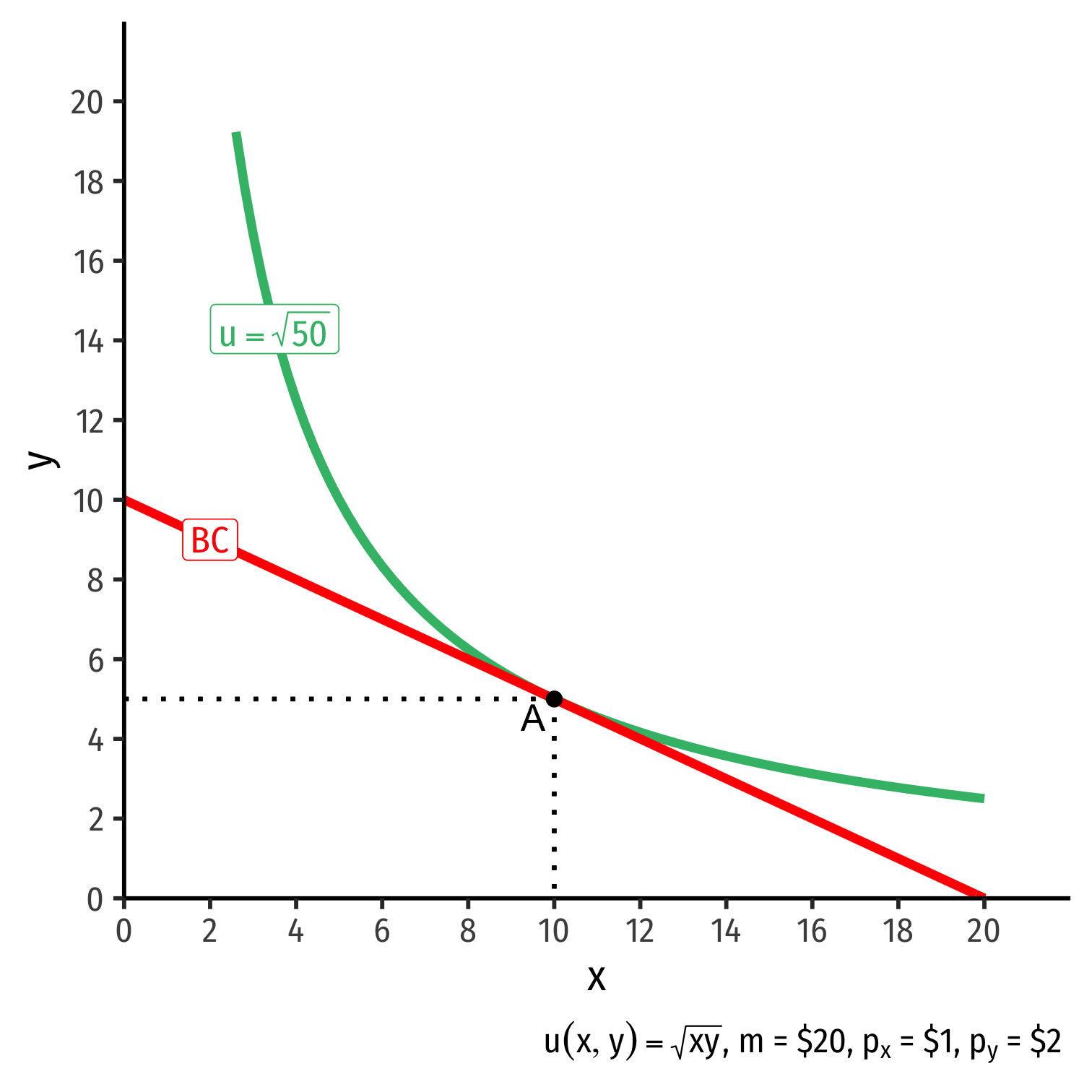

The Consumer's Optimum: Why A?

indiff. curve slope=budget constr. slope

The Consumer's Optimum: Why A?

indiff. curve slope=budget constr. slope|MRSx,y|=|pxpy||MUxMUy|=|pxpy||−0.5|=|−0.5|

Consumer would exchange at same rate as market

No other combination of (x,y) exists at current prices & income that could increase utility!

The Consumer's Optimum: Two Equivalent Rules

Rule 1

MUxMUy=pxpy

- Easier for solving math problems (slope of each curve)

The Consumer's Optimum: Two Equivalent Rules

Rule 1

MUxMUy=pxpy

- Easier for calculation (slopes)

Rule 2

MUxpx=MUypy

- Easier for intuition (next slide)

The Consumer's Optimum: The Equimarginal Rule III

Any optimum in economics: no better alternatives exist under current constraints

No possible change in your consumption that would increase your utility

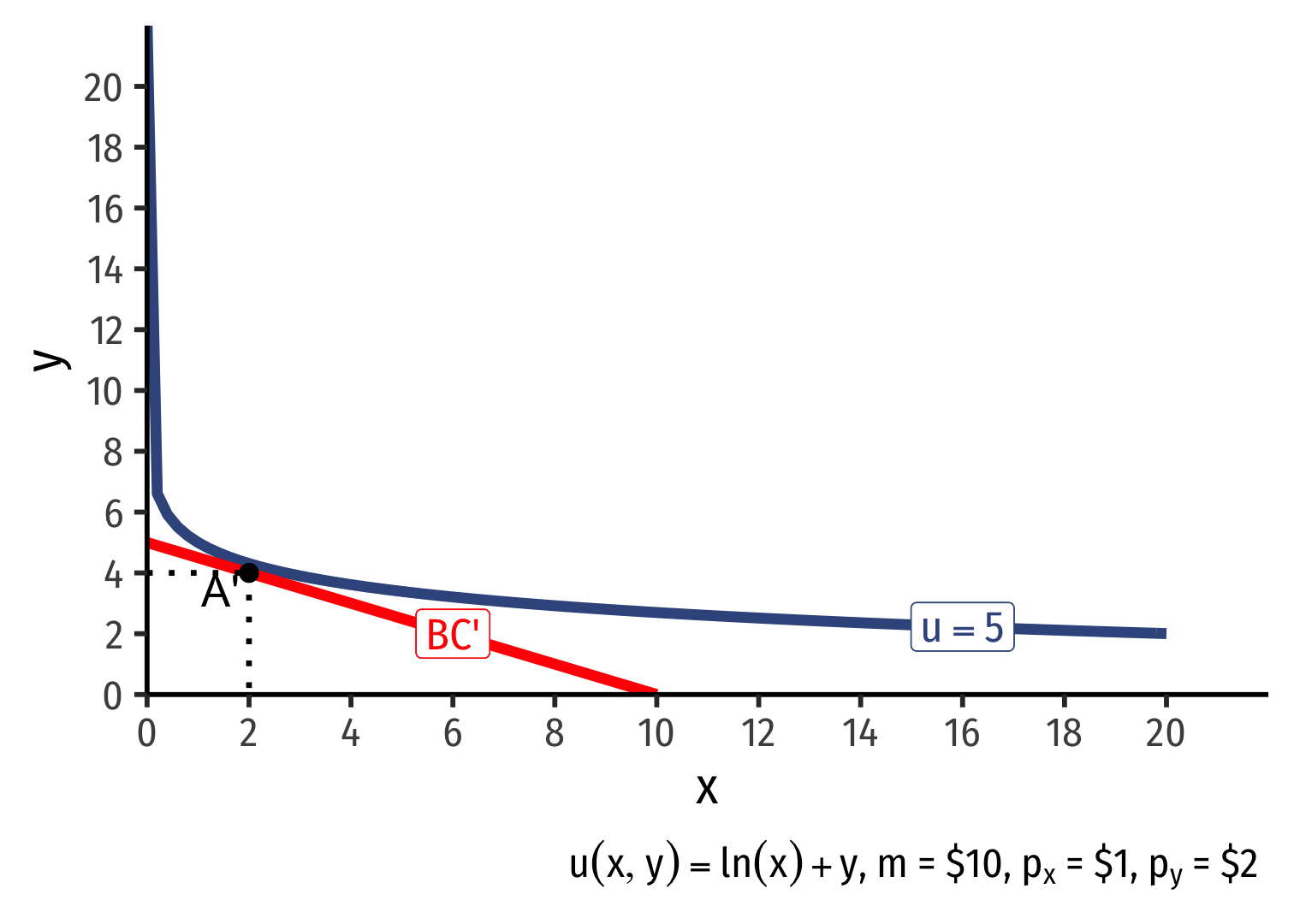

Markets Equalize Everyone's MRS I

Markets make it so everyone faces the same relative prices

- Budget constraint. slope, −pxpy

- Note individuals' incomes, m, are certainly different!

A person's optimal choice ⟹ they make same tradeoff as the market

- Their MRS = relative price ratio

markets equalize everyone's MRS

Markets Equalize Everyone's MRS II

Two people will very different income and preferences face the same market prices, and choose optimal consumption (points A and A') at an exchange rate of 0.5Y:1X

Optimization and Equilibrium

If people can learn and change their behavior, they will always switch to a higher-valued option

If a person has no better choices (under current constraints), they are at an optimum

If everyone is at an optimum, the system is in equilibrium